This is Information Sheet 178 (INFO 178). It summarises the findings in REP 331 and what they mean for investors and listed entities.

On 18 March 2013, ASIC released Report 331 Dark liquidity and high-frequency trading (REP 331) and Consultation Paper 202 Dark liquidity and high-frequency trading: Proposals (CP 202), examining the impact of dark liquidity and high-frequency trading on Australia’s financial markets. These publications were the result of analysis by two internal ASIC taskforces.

Download as a PDF file (115 KB)

Overall, we did not find any fundamental deterioration of market quality or systematic abuse that threatens the integrity of our market. In fact, we found that the Australian market is generally of high quality and integrity. Where we did find issues:

- we have worked with industry to remedy the issues where possible

- our Enforcement teams are investigating a number of possible breaches of rules

- we have proposed a number of new rules and guidance in CP 202, which we are consulting on until 10 May 2013.

What are dark liquidity and high-frequency trading?

Dark liquidity

Investors typically trade securities on ‘lit’ exchange markets, such as ASX and Chi-X. On these markets, buy and sell orders are visible and accessible to the rest of the market, before they are executed.

Dark liquidity refers to buy and sell orders that are not visible to the rest of the market, although the trades are typically published immediately after they take place. Dark trades are usually done away from exchange markets and are accessible only to a subset of the market (e.g. often limited to a market participant and its clients). There are also dark trading venues known as ‘dark pools’ or ‘crossing systems’. A dark pool is a system that enables trading away from lit exchange markets. A crossing system is a dark pool which is operated by a market participant (a participant of a licensed market, with permission to directly access the market to trade on behalf of their clients and/or themselves).

High-frequency trading

High-frequency trading is not a technical term. High-frequency traders, like many other traders in our market, use computer algorithms to generate buy and sell orders on markets such as the ASX and Chi-X. These orders can be entered and amended a lot faster than orders generated by people. High-frequency traders tend to trade on both sides of the market, to profit from incremental price differences, rather than to look for underlying value.

Why is ASIC examining dark liquidity and high-frequency trading?

In recent years, there have been significant structural and behavioural changes in Australia’s financial markets. Our markets have become increasingly automated and innovative. We also now have competition between licensed equity markets.

Advances in technology have made it easier to trade away from exchange markets and have facilitated a proliferation of dark trading venues—there are currently over 20 dark venues. Trade on these dark venues is mostly in the 200 largest, and most liquid, securities.

Technological advances have also driven the shift to algorithmic trading, where orders are generated and executed in fractions of a second, managed by pre-programmed computer algorithms. Dark liquidity and high-frequency trading have been the subject of significant public commentary, both in Australia and overseas:

- Dark liquidity: There are concerns that the nature and use of dark liquidity are changing and that these changes are affecting the prices of securities. There are also questions about the fairness of dark venues for investors, with concerns that they are not regulated as markets and ‘free ride’ on the pricing and information set on ‘lit’ exchange markets.

- High-frequency trading: There are questions about the value that high-frequency trading brings to market quality. There are concerns about the ‘noise’ created by excessive trading messages that relate to small and/or fleeting orders (messages which make it more difficult to discern significant trading patterns), and concerns that high-frequency traders employ predatory strategies or that they ‘game’ the orders of fundamental investors, manipulate prices and may contribute to market instability.

In mid-2012, ASIC established two internal taskforces to consider the impact of these developments on the quality and integrity of Australia’s financial markets. Our focus has been on the interests of fundamental investors (investors who buy or sell securities based on an assessment of their intrinsic value; also known as ‘long-term investors’) and listed entities looking to raise capital in the market, and on Australia’s competitiveness as a regional financial centre.

Dark liquidity

Findings

There is an inherent tension between:

- the short-term private advantages for a subset of the market of trading in the dark (e.g. lower exchange fees paid by brokers and potential price improvement for investors), and

- the long-term public good of contributing to the price formation process, which gives investors confidence and promotes the interests of listed entities and the broader community through an efficient secondary market for capital.

Dark trading in our market

In allowing trading in the dark, ASIC’s (and the ASX’s) regulatory intent was to minimise the impact on the market of very large trades. However, while the proportion of trading that occurs in the dark has remained relatively constant (at about 25–30% of total equity market turnover), the nature and purpose have changed.

There has been a shift in dark trading away from large block size trades (i.e. over $1 million) to trades in smaller sizes. In September 2012, large block size trades accounted for just 10% of total equity market turnover (i.e. value) compared with 14% in September 2011. There was a decrease in the number of block size trades from 32,000 trades to 10,000 over the period. This compares with dark trades below block size for the same period, which increased from 9% to 14% of total equity market turnover (i.e. value), while the number of trades grew by 388% from 670,000 to 2.6 million.

Dark trades are much smaller in size than they used to be and are now very similar in size to trades on lit exchange markets. For example, the median dark trade size was $400 in September 2012. This means that half of dark trades were $400 or smaller. We expect this is a result of trading algorithms programmed to break larger orders into many small orders.

There appears to be less trading by fundamental investors, including retail investors, on lit exchange markets. For example, of the brokers that deal with the majority of retail orders, dark trades accounted for 11% of their total trading (by value) in September 2012 – up from just 4% in September 2010.

Impact of dark liquidity on prices of securities

We found that growth in dark trading has contributed to a widening of bid–offer spreads (i.e. the difference between buy and sell prices) in some securities. We found that this has affected price formation for these securities. This correlation is strongest in the 200 largest and most liquid securities (i.e. the S&P/ASX 200).

A new market integrity rule commencing on 26 May 2013 is expected to help address this adverse impact of dark liquidity on prices. The new rule will require all dark trading to be done at a meaningfully better price than is available on a lit exchange market. Otherwise, the trade must be done on a lit exchange market. Canada introduced a similar rule in October 2012 and has seen a significant decline in the volume of dark trading.

We have also proposed a safety net in CP 202. If dark liquidity continues to increase and to affect prices and depth, we will introduce a minimum dark order size of $20,000 (or $50,000 for the largest securities). This will mean that orders below these sizes would need to be traded on a lit exchange market.

Separately, we found that the minimum price increment (tick size) at which a security can trade (e.g. 1c for most securities) may lead to increased trading in the dark. Where there are lots of buy and sell orders waiting in the queue of orders on a lit exchange market at the best prices, it is possible to jump the queue by trading in the dark. This queuing problem is most common in low-priced, highly liquid securities (e.g. Telstra). We are seeking feedback in CP 202 on two options for addressing this problem.

Dark trading venues

There are over 20 dark trading venues operating in Australia. ASX operates one – Centre Point – which is accessible to all market participants. There are a further 20 dark venues operated by 16 brokers. These broker venues are typically only accessible to clients and have evolved from the brokers’ manual dealings between clients.

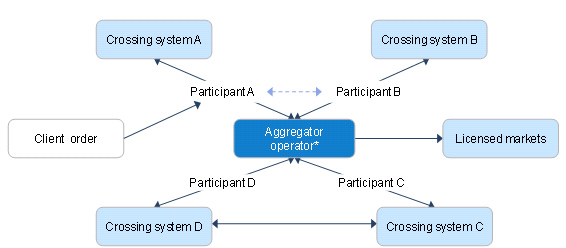

These broker dark venues have started to connect to one another. A client of one broker may find its order is matched on the venue of another broker, even if it has no relationship with that other broker: see Figure 1. This means that these broker venues are becoming increasingly ‘market-like’.

Figure 1: Examples of linkages between crossing systems

We found that, overall, there is limited transparency in the wider market, and there has been selective disclosure to users, about the operation of crossing systems, the trades that are done in crossing systems and about who participates in crossing systems (e.g. there is limited information about the prevalence of high-frequency trading or about trading by the broker as principal).

- We have heard from investors that they want more information about how and where their orders are executed; and we have heard from entities that they need to understand where their securities are trading and who is trading them.

- We found that high-frequency traders are active in crossing systems. Around 5% of high-frequency trading equity market turnover is done in the dark.

- A substantial proportion (38% in September 2012) of trading in broker crossing systems is the broker trading as principal – that is, the broker itself was on one side of the trade as either the buyer or seller for more than $1 in every $3 traded. This raises considerable potential for conflicts of interest.

We also identified circumstances where brokers appear to be unduly favouring some clients over others, there is limited monitoring of trading in crossing systems by brokers, and there are limitations with brokers’ systems and controls.

Broker crossing systems are here to stay. It is important that they are appropriately regulated. We have proposed a number of rules to address the issues identified:

- On transparency and disclosure, we have proposed that clients should be informed when trades have been done on a crossing system, and when the counterparty was the broker acting on its own behalf. Information about the operation of the crossing system should be made publicly available. Course-of-sales reports will uniquely identify trading venues, including dark venues, for each trade. These reports will be published three days after a trade.

- We have proposed rules to ensure there is no undue discrimination between clients, and clients must be able to opt out of using a crossing system.

- We have proposed minimum expectations about brokers monitoring activity on their crossing systems.

- We have proposed enhanced systems and controls.

Treasury is also considering changes to the market licensing regime that may affect dark pools.

Conflicts of interest

There are inherent conflicts of interest with brokers handling client orders, particularly when a broker trades with clients against its own account. We have proposed in CP 202 to enhance conflicts of interest obligations (e.g. for protecting client information when outsourcing services, and for brokers to give client orders priority over their own orders when trading as principal).

We have also observed in overseas markets the emergence of a practice known as ‘payment for order flow’. This is where an entity receives a payment from a broker for sending its clients’ order flow to the broker. These payments can influence how and where client orders are directed and create significant conflicts of interest. We have proposed to prevent these payments for order flow.

What does this mean for investors?

The new rules relating to dark liquidity are designed to provide more choice to investors about how and where their orders are executed, while at the same time providing sufficient investor protection from the impact of conflicts of interest and poor transparency that may result from excessive dark trading.

The new rules address two key problems for investors:

- the negative impact on the price investors pay for securities caused by excessive dark trading

- the lack of information and access for investors to exercise informed choices about where their orders are executed.

How is the risk of price deterioration addressed?

Excessive dark trading can affect the price investors pay for securities. Prices are most efficient when there is optimal interaction between supply and demand. There is the risk that, as more order flow of fundamental investors is directed away from exchange markets, the quality of the prices on the exchange market deteriorates (i.e. wider bid–offer spreads and possibly less volume at each price).

We believe the existing measures, including the new price improvement rule that commences in May 2013, will address the risk of deterioration to prices.

The proposed trigger for a minimum dark order size provides an additional safety net for investors.

Commencing in May 2013, the minimum block trade size (i.e. the point at which trades can occur at any price in the dark) will be reduced from $1 million to $200,000 for the vast majority of securities. This should provide investors with more flexibility to trade in larger (rather than small) sizes in the dark.

Investors and their brokers

The proposed new rules supplement existing investor protections, including obligations for brokers to deliver best execution (i.e. the best possible outcome) for their clients.

These proposals are intended to give investors more comfort that, if they choose to trade in the dark, there are controls and protections around those trades.

However, investors should also ask more questions of their broker(s) and provide specific instructions if they are seeking specific outcomes.

What does this mean for listed entities?

Listed entities have limited visibility of where their securities are traded when this occurs in the dark. Excessive dark trading can produce or amplify the following corporate risks:

- wider bid–offer spreads, which in turn may lead to more volatile prices

- increased volatility, which may make capital raising more costly.

Our proposals on transparency will provide listed entities with more visibility of where their securities are being traded.

As noted above, the combination of existing and new measures will protect the integrity of the price formation process and help to keep bid–offer spreads tight.

High-frequency trading

Because high-frequency trading is not a technical term, definitions can vary. While it is often equated with algorithmic trading – and high-frequency trading is indeed a type of algorithmic trading – not all forms of algorithmic trading can necessarily be described as high-frequency.

An algorithm is simply pre-programmed logic that allows the creation, or amendment, of an order when a ‘signal’ is received, such as a security trading at a given price level. A simple algorithm may be a ‘stop-loss’ strategy, where a market order is generated when a specific security trades at the trigger or ‘stop-loss’ price.

Algorithms used by high-frequency traders are considerably more sophisticated and are able to quickly process information from a variety of sources in order to make trading decisions for that particular strategy (i.e. the price and volume for an order that should be entered, amended or cancelled).

High-frequency traders are generally risk averse, and therefore do not open and hold large positions in the market. They tend to operate on a low margin, and maintain bids and offers at the current market prices and in the most liquid securities, thereby earning the spread as many times as possible to ensure maximum profitability.

Many investors and securities dealers exhibit a number of the same trading attributes as high-frequency traders, using sophisticated technologies for trading. For example, many algorithms executing ‘buy-side’ strategies share some of the characteristics of high-frequency trading.

Our analysis of high-frequency trading

We analysed data from our surveillance feed from ASX and Chi-X to identify the nature and extent of high-frequency trading in the Australian market. More broadly, we also engaged with industry and regulators both here and overseas, reviewed relevant research, and identified regulatory gaps.

We conducted a detailed analysis of trading on equity markets over the nine-month period from January to September 2012. This analysis drew on a number of measures that could be consistently and objectively measured, and that related strongly to the characteristic attributes of high-frequency trading. These included order-to-trade ratios, percentage of turnover traded within the day, total turnover per day, the number of fast messages, holding times, and at-best ratios.

Findings

Our analysis showed that, while there is a considerable high-frequency trading presence in our markets – 27% of equity market turnover – the majority of it is done by 20 entities.

On the whole, we found that some of the commonly held negative perceptions about high-frequency trading appear to have been overstated, and were not supported by our findings. For example, the taskforce found that increases in order-to-trade ratios have been moderate compared with overseas markets, and have not been driven entirely by high-frequency trading.

Our analysis also showed that only 1.2% of high-frequency traders held positions for an average of two minutes or less, 18% for less than 10 minutes, and 51% for less than 30 minutes. This is contrary to the perception that holding times for high-frequency traders are typically a matter of seconds, or less.

We also found no evidence of systematic manipulation, or other predatory behaviours, from high-frequency traders, and while a number of discrete incidents required follow-up, these were the exception rather than the norm.

There was, however, some basis for the perception that high-frequency trading created excessive ‘noise’ in the market, although our analysis revealed that other traders using algorithms contributed to this problem.

Current regulatory framework and proposals

A principal concern, held by all regulators, about algorithmic trading, is the inadvertent interaction of a number of programs on the market that may result in the event of significant market disorder, as happened in the 2010 ‘flash crash’ in the United States.

Over the past three years, since ASIC became the frontline supervisor of Australian licensed markets, we have developed a robust regulatory framework of rules and guidance to address electronic trading. New market integrity rules for automated trading have been introduced to supplement the existing rule framework, and further rules will take effect over the next 12 months.

These new rules are designed to strengthen the regulatory regime and further mitigate against market disorder. They enhance market operator controls for extreme price movements, and market participant filters and controls for automated trading. These will include a ‘kill switch’ to immediately shut down problematic algorithms.

As a result, we found that minimal additional requirements were necessary. Our attention was focused on other market quality issues.

We are proposing to introduce a rule to reduce the market noise from small and fleeting orders that offer little economic utility by stipulating the time such orders must remain in the market before being amended or cancelled.

We are also proposing to introduce guidance on order-to-trade ratios. Although we did not conclude that there are systemically problematic levels currently in our markets, we want to ensure that our participants remain vigilant about the order-to-trade ratios their clients are exhibiting, and to ensure these do not become excessive.

We have seen that some behaviours exhibited by high-frequency and other algorithmic traders are perceived to be manipulation. We are confident that our current market misconduct provisions adequately restrict manipulation.

Nevertheless, we are proposing a further amendment to existing market integrity rules prohibiting manipulative behaviours, to include additional circumstances when placing orders to avoid an implication of manipulative trading behaviour.

We also intend to issue guidance on the types of trading behaviours and conduct ASIC would consider to be manipulative.

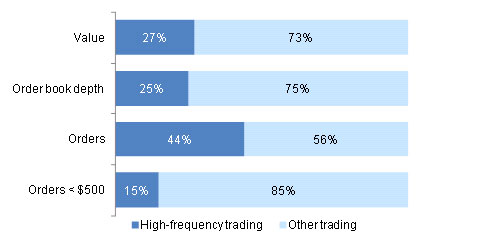

As illustrated in Figure 2, when considering the presence of high-frequency trading in our market, we found that algorithms are used extensively in buy-side execution. The analysis revealed that there are more orders, and significantly smaller orders, by non-high-frequency trading algorithms, illustrating the extensive use of algorithms by the buy-side.

Figure 2: Presence of high-frequency trading in our market

We also found that high-frequency trading in Australia is dominated by a small number of trading entities. Our analysis of trading on Australian securities exchanges in the period January to September 2012 revealed that just 20 trading entities accounted for 80% (by turnover) of all high-frequency trading (and 22% of all equities markets turnover) in that period.

We also found that high-frequency trading in Australia is dominated by a small number of trading entities. Our analysis of trading on Australian securities exchanges in the period January to September 2012 revealed that just 20 trading entities accounted for 80% (by turnover) of all high-frequency trading (and 22% of all equities markets turnover) in that period.

ASIC understands that technological advances in the markets will continue. As a result, we will continue to monitor and supervise the markets, and market behaviour, and take action where required.

What does this mean for investors?

The proposals in CP 202 and also our report on dark liquidity and high-frequency trading should improve the quality and integrity of our markets and enhance investor confidence. Our analysis shows that, in general, high-frequency traders are not manipulating the market or systematically ‘gaming’ investors.

Our markets have changed, algorithms have reduced trade sizes and a large proportion of trading is done by professional traders who would not be described as long-term investors. Developments in automated trading have been by far the largest contributor to this change, and this has been from all facets of the industry including the buy-side.

While we feel it is important that this evolution is understood, we do not believe there should be widespread concern about the next evolutionary stage because there are many positive outcomes attributed to automated trading enjoyed by the investing community, including greater liquidity and depth, and narrower bid–offer spreads in many securities.

What does this mean for listed entities?

Concerns raised by listed entities about high-frequency trading contributing to share price volatility were not supported by our findings. In addition to our market-wide analysis, we examined a number of cases presented to us by listed entities. In most cases, we found that the movement in prices was driven by algorithms of long-term investors rather than high-frequency trading.

We have proposed a rule to require small fleeting orders to rest for a minimum time on the market before they can be cancelled or amended. This was proposed in response to concerns that large volumes of small orders and trades may disguise genuine trading interest and create ‘noise’ for the market. While ASIC believes this will help address the issue, we are acutely aware of the fact that algorithms have become part of the norm in our market, with orders and trade continuing to be a feature of it.

Listed entities should note that our findings indicated that high-frequency traders tend not to hold positions overnight and therefore do not appear on share registers. Given the transitory nature of high-frequency traders’ investment in a listed entity, we believe that these traders do not need to be a focus for a listed entity in complying with its disclosure obligations.

For further information, contact ASIC at marketstructure@asic.gov.au.

Important notice

Please note that this page is a summary giving you basic information about a particular topic. It does not cover the whole of the relevant law regarding that topic, and it is not a substitute for professional advice. You should also note that, because this information sheet avoids legal language, wherever possible, it might include some generalisations about the application of the law. Some provisions of the law referred to have exceptions or important qualifications. In most cases, your particular circumstances must be taken into account when determining how the law applies to you.

Information sheets provide concise guidance on a specific process or compliance issue or an overview of detailed guidance.

This information sheet was reissued in January 2014.