ASIC’s priorities for the supervision of market intermediaries

ASIC's priorities for supervising market intermediaries are intended to help you assess your risk management framework and focus your compliance, supervisory and risk management efforts.

2025-26 priorities for supervising market intermediaries

ASIC’s strategic priorities are detailed in ASIC’s Corporate Plan 2025-26.

In our supervision of market intermediaries, ASIC will focus on five strategic priorities:

- Improve consumer outcomes

- Strengthen market disclosure and professional conduct

- Support better retirement outcomes and member services

- Strengthen operation digital and data resilience and safety, and

- Drive integrity and transparency across markets.

Our Corporate Plan and strategic priorities are shaped by the opportunities and challenges of Australia’s evolving financial landscape, including changing capital markets, technological transformation, uncertainty and resilience and superannuation growth and risk of exploitation.

Outlined below are the key projects and regulatory activities ASIC’s Markets Group will undertake this year to advance our strategic priorities.

![]()

Drive integrity and transparency across markets

In the last year, ASIC has examined and advanced discussion on issues shaping the future of Australia’s public and private markets and ASIC’s regulatory approach. We released a Discussion Paper in February 2025 and met with a wide range of industry participants and representatives through panels, forums, a symposium and various other engagements. We shared industry feedback in June and provided an update on our work in September.

In 2025-26, our continuing work to drive integrity and transparency across markets includes:

- Public and private markets: In November 2025, we will unveil ASIC’s roadmap for strong, efficient and globally competitive public and private markets. This work is built on stakeholder submissions and engagement, expert insights, our surveillance and other actions taken since February.

- Public markets: ASIC will continue to support the health and future of Australia’s public markets. While we do not see regulatory settings as the dominant factor driving listing decisions in Australia, we have already made adjustments to improve the attractiveness of Australia’s listed equities markets, including changes to streamline the IPO process (25-096MR). We have commenced initial stakeholder engagement on our guidance in Regulatory Guide 264 Sell side research (RG 264) and are open to considering further ideas to support public markets, including on pre-prospectus advertising, prospectus length and trading plans.

- Private markets: In the past decade, private markets have rapidly expanded to unlock new investment opportunities across companies, innovative ventures and infrastructure projects. In response to the pace of growth, ASIC commissioned a paper on Australia’s private credit funds sector, Report 814 Private credit in Australia (REP 814). Responses to the discussion paper and REP 814 confirmed our view that the growing availability of private capital has met a real need. If ‘done well’, private credit is good for investors, borrowers and the economy, complementing the banking system and providing further opportunities for innovation, employment and growth.

- ASIC has conducted surveillance on the private credit funds sector, and our early findings align with the insights on better and poorer practices in REP 814, particularly those relating to valuations, liquidity and transparency. In November 2025, we will release findings from ASIC’s private credit surveillance across retail and wholesale funds. We will outline principles – anchored in existing regulation – for sound private credit practices that provide a clear basis for assessing practices, improving and to build trust and confidence.

- Superannuation: We will continue to include superannuation trustees in our surveillance of market cleanliness, financial reporting and audits, and investment disclosures, including our work in the platforms segment. In conjunction with APRA, ASIC will continue to review the superannuation funds’ investments in private markets and their valuations of illiquid assets. We will also conduct a review of superannuation trustee practices to better understand the steps they have taken to disrupt the high-risk super switching model.

- Data and transparency: In conjunction with other relevant local and global regulators, ASIC is reviewing the private markets data provided to regulators, to ensure flows, exposures and potential systemic risks are better understood and managed.

- Enhancing market integrity: Our real-time and post-trade surveillance of trading on Australia’s domestic licensed markets utilises our award-winning technology and significant expertise to identify insider trading, market manipulation, continuous disclosure breaches, disorderly trading and misinformed markets. These are enduring enforcement priorities. We are developing new tools to increase our detection of complex and novel market misconduct matters, market microstructure manipulation and breaches of the market integrity rules. We continue to focus on short position reporting and regulatory data compliance.

- Market cleanliness and confident participation: We continue to scrutinise corporate finance transactions for misleading or deceptive statements, and conduct contrary to the Corporations Act, to support market integrity and shareholder protection. Our oversight of market cleanliness includes monitoring of anomalous trading ahead of material price sensitive announcements, including corporate finance and takeover transactions. We are also exploring market cleanliness around trading activities in government and semi-government bonds and are enhancing our monitoring of cleanliness to adapt to changing market dynamics, especially the rise in private market investing. We may undertake a review and publish a Report on market cleanliness within private market transactions. We will continue to facilitate access to markets with equivalent shareholder protections and market integrity standards to enhance opportunities for retail participation in public markets.

- Pre-hedging: Following conclusion of IOSCO’s work and publication of its final report on pre-hedging, we will consider how to apply the recommendations in Australia. In addition to proposed recommendations to regulators on effective management of conduct risks when pre-hedging – topics addressed in ASIC’s February 2024 guidance on pre-hedging – IOSCO’s consultation report proposed a definition of pre-hedging and recommendations regarding the appropriate use of pre-hedging.

- Digital assets and innovation in financial markets: We will finalise updates to our guidance on digital assets and related products, support Treasury with law reform and transition, and support the Australian central bank digital currency pilot for digital financial innovation. We will continue to look for opportunities to support responsible innovation in the financial sector, including through our Innovation Hub and the enhanced regulatory sandbox and continue our work on the future of tokenisation and decentralised finance.

Our work to drive integrity and transparency across markets will in many ways also contribute to achieving our strategic priority to support better retirement outcomes and members services.

![]()

Improve consumer outcomes

We are concerned about people potentially risking their investments and retirement savings in complex schemes or high-risk products as a result of high-pressure sales tactics and inappropriate advice.

In 2025-26, we will work to drive better outcomes for consumers of financial products and services, including:

- CFD sector report: Publish a report setting out our key findings, outcomes and remediation from a sector-wide review of CFD issuers’ distribution practices and compliance measures.

- Mis-selling of complex products: We will undertake a thematic review of distribution practices and potential mis-selling of high-risk or complex financial products to retail clients, SMSFs and ‘sophisticated investors’. We will continue to disrupt unlicensed conduct, fraud and scams through takedowns of scam websites and adding unlicensed and imposter entities to Moneysmart’s investor alert list.

- Product intervention: ASIC’s CFD product intervention order is due to expire on 23 May 2027, unless remade. In 2026, we will consult on our proposed way forward.

Digital engagement practices: We are designing a trading simulation tool to educate consumers of potential harms associated with digital engagement practices and dark patterns. We also plan to clarify the Australian financial services licensing and compliance arrangements required to provide copy trading services to clients.

![]()

Strengthen operational digital and data resilience and safety

New and evolving technologies continue to rapidly transform our financial system. Additional pressures from geopolitical tensions, cyber threats and an uncertain global economic outlook, resilience is necessary to withstand and adapt to unfolding events while minimising disruption. Our work under this strategic priority aims to minimise instability, technology, cyber and data-related risks across our markets.

- Inquiry into the ASX: We are conducting an inquiry into the ASX group, led by a panel of experts, focusing on governance, capability and risk management frameworks and practices. The panel will make recommendations to address any shortcomings or deficiencies identified. We will publish a report on the outcome of the inquiry in March 2026 and encourage prompt implementation of the recommendations. For more information about the scope of the Inquiry, refer to the Terms of Reference.

- Market infrastructure: While the ASX Inquiry is underway, it is critical ASX continues to prioritise the safe and efficient operation of its infrastructure, including progress towards Release 1 of the CHESS replacement project by mid-2026. The expert technical review of CHESS, that ASIC announced on 31 March 2025, will continue alongside the Inquiry. ASIC will continue to closely monitor this project, and our oversight of the ASX Group will evolve with the Inquiry recommendations. We will also continue work to implement financial market infrastructure reforms, consulting on updated guidance in 2026.

- Market stress control settings: We will review the suitability of our regulatory settings for significant market events. Our review will consider the effectiveness extreme stress control mechanisms for today and into the future.

- Crisis preparedness: We will work to ensure our preparedness for geopolitical and significant crisis events through a range of actions, including participation in the Council of Financial Regulators’ work on geopolitical risk.

- Cyber and operational resilience: Our focus will be on promoting good practices for managing risk, incident response and communications, increasing the engagement and resilience of regulated entities and their customers, and cross-agency collaboration.

- Outsourcing review: We will review market participants’ compliance with market integrity rules on managing outsourcing arrangements and test reliance on third-party vendors, including those widely used but not regulated as providers of financial services.

- Modernise MIRs for trading systems: We will consider feedback and finalise proposals to Consultation Paper 386 Proposed amendments to the ASIC market integrity rules: Trading systems and automated trading (CP 386) to modernise, streamline and harmonise ASIC market integrity rules (MIRs) governing market participants’ trading systems and automated trading. As part of this consultation, we invite further suggestions of ways to simplify and improve the MIRs.

IMF financial sector assessment: We will contribute to the International Monetary Fund Financial Sector Assessment Program (FSAP) review of Australia during 2025–26. The FSAP evaluate the quality of supervision and regulation and includes analysis of the resilience of Australia’s financial sector and stress testing of its financial institutions.

![]()

Strengthen market disclosure and professional conduct

ASIC’s work in this area aims to strengthen market disclosure foundations and conduct by regulated professionals, with a focus on:

- Financial reporting: We will proactively review financial reports and audits and act against entities, including large proprietary companies, who do not comply with obligations to lodge financial reports.

- Climate reporting: We will take a pragmatic and proportionate approach to supervision and enforcement of the sustainability reporting obligations.

- Auditor independence: We will continue to examine auditors’ compliance with their independence and conflicts of interest obligations and publish our surveillance findings.

- Director conduct: We will review the arrangements that companies have in place to manage conflicts of interest by directors and officers and how they are applied, particularly in times of corporate distress.

Independent Expert Reports: We will act to protect investors where we identify concerns regarding the quality of expert reports, or the capacity of expert licensees to meet their obligations in providing these reports.

Regulatory simplification

We are focusing on what we can do, within ASIC’s powers, to address regulatory complexity.

In September 2025, we published our Report 813 Regulatory simplification (REP 813). The report sets out our progress and seeks feedback on initiatives we are undertaking as part of a multi-year program focused on:

- Improving access to regulatory information

- Reducing complexity in regulatory instruments

- Making it easier to interact with ASIC

- Supporting simplification through law reform.

As well as specific project work, we continue to engage with CFR agencies, industry associations and market participants. We aim to embed simplification as a key part of how we work day-to-day and interacting with our stakeholders. We continue to welcome your suggestions relevant to our simplification work.

Core regulatory activities

In addition to these projects aligned to our strategic priorities, ASIC will continue its core regulatory activities to monitor and promote market integrity and confident and informed participation by investors. We do this by:

- conducting supervision and surveillance to identify emerging risks, test compliance and enhance market conduct and consumer outcomes

- issuing guidance about how we plan to administer the law

- granting relief from regulatory requirements to facilitate business, promote innovation and support the Australian economy

- engaging and educating consumers through the Moneysmart website

- taking strong enforcement action targeted to have the greatest impact on the most serious harms and misconduct in our remit, guided by our strategic and enforcement priorities.

Uphold fairness, honesty and professionalism: We conduct surveillances to identify and understand emerging risks, test compliance with the law and enhance market conduct and consumer outcomes. When our surveillances identify misconduct within our jurisdiction, we will consider regulatory, administrative or enforcement action to protect consumers and promote market integrity.

Conclusion

Australia’s financial markets are strong, and they are adapting to meet the future needs of our economy. As a modern, confident and ambitious regulator, ASIC remains committed to the promotion of market integrity, resilience and fair, honest and professional business practices fundamental to maintaining trust and confidence in Australia’s financial system.

We encourage you to use these strategic priorities, projects and regulatory activities as a reference for your compliance, supervisory and risk management programs that support your business activities, and to prepare for your interactions with ASIC.

Past priorities for supervising market intermediaries

Below are ASIC's priorities for supervising market intermediaries for the past five financial years.

Priorities for 2024-25

ASIC’s strategic priorities are detailed in ASIC’s Corporate Plan 2024–25.

In our supervision of market intermediaries, ASIC will focus on five strategic priorities:

- Improve consumer outcomes

- Address financial system climate change risk

- Better retirement outcomes and member services

- Advance digital and data resilience safety, and

- Drive consistency and transparency across markets.

Our Corporate Plan and strategic priorities are shaped by the opportunities and challenges of our external environment, including rapid technological transformation, cost of living pressures, climate change, an ageing population and evolving financial market dynamics.

This year ASIC will undertake a wide range of key projects and regulatory activities outlined below to deliver on our strategic priorities.

Drive consistency and transparency across markets and products

In 2024–25, a new strategic priority—focused on driving consistency and transparency across markets and products—underscores ASIC’s commitment to strengthening integrity across Australia’s markets.

The dynamic between public and private financial markets continues to evolve. Global trends include reductions in the numbers of initial public offers and listed companies, the scale and growth of superannuation and pension funds, digital transformation, disintermediation, and the rapid growth of private equity, private credit and other alternative investments.

To drive consistency and transparency across markets and products, we will:

- examine changes in public and private markets for equity and debt capital, including the significant growth of private markets and the implications for the integrity and efficiency of markets

- engage with industry, monitor international developments and facilitate discussion about regulation of capital raisings and equity and debt capital market efficiency, transparency and resilience

- enhance monitoring and reporting on our markets’ cleanliness, expanding beyond equity markets

- engage with market stakeholders on our pre-hedging guidance, conduct thematic reviews to assess trader practices to raise and harmonise minimum standards of conduct, and promote fair competition and the effective functioning of markets

- conduct thematic reviews of corporate advisers and private finance funds, including governance, valuation practices, management of conflicts of interest, staff and insider trading, protection of confidential information and fair treatment of investors

- actively target leaks of confidential information and review the confidentiality protections of parties involved in public and private market transactions. Leaks undermine market integrity and may negatively impact the attractiveness of Australian markets as a place to raise capital and transact

- establish a specialist insider trading team to expedite insider trading investigations and increase the number of criminal briefs we refer to the Commonwealth Director of Public Prosecutions

- supervise and support integrity and fairness in energy commodity and carbon credit markets (further described in our work to address financial system climate change risk)

- provide guidance on, and implement, the ASIC Derivative Transaction Rules (Reporting) 2024 in October 2024

- make clearing and settlement services rules to support ASX in fostering competition for clearing and settlement and aim to facilitate outcomes that are consistent with those that are expected in a competitive market for clearing and settlement services, and

- enhance our guidance and processes for supervising the conduct of financial market infrastructure providers.

Our work to drive consistency and transparency across markets and products will in many ways also contribute to achieving our strategic priority to support better retirement outcomes and members services.

Improve consumer outcomes

We will work to drive better outcomes for consumers of financial products and services, with a focus on:

- the design and distribution of financial products

- predatory sales practices

- disruption of online investment scams

- alerting investors to unlicensed conduct through Moneysmart, and

- dispute resolution.

With a market’s focus, we will:

- review consumer outcomes from emerging methods of complex product distribution to retail clients,

- disrupt and take action against misleading or deceptive conduct and misinformation relating to investment products. This will include advertising or digital engagement practices that obscure the risk, performance or nature of financial products, and

- consider vulnerabilities that may lead to share sale fraud, amplify understanding of the potential for harm of control failure in this area and encourage better practices by market intermediaries.

Address financial system climate change risk

Market intermediaries and financial sector organisations are increasingly grappling with climate-related risks. With the growth of sustainability-related investment, there is increased risk of poor disclosure and greenwashing, including using net zero statements and other sustainability-related claims. These can have a negative impact on efficient capital markets.

As we move towards a net zero emissions target, ASIC will support market integrity and protect consumers and investors, with a focus on:

- climate-related disclosure

- greenwashing (see REP 763), and

- integrity and fairness in energy and carbon credit markets.

Over the next 12 months, to support sustainability and Australia’s energy transition, we will:

- continue to support the introduction of the mandatory climate-related financial disclosure requirements for large Australian businesses and financial institutions through updated guidance and consultation

- support fair and efficient carbon markets and products through effective oversight, licensing and supervision

- update policy and guidance on regulating carbon-based financial products to provide clarity on disclosure

- contribute to the formation of global carbon market standards and consistency through our work with IOSCO and other international regulators

- monitor new and established markets for carbon-related financial products (such as Australian Carbon Credit Units) to ensure markets and intermediaries are meeting expectations and standards

- undertake surveillance activity and take enforcement action, where necessary, to prevent harms from greenwashing and other sustainable finance-related misconduct, and

- conduct surveillance of market intermediaries’ commodity and energy derivatives trading and supervisory functions.

Advance digital and data resilience and safety

New and evolving technologies continue to transform our financial system. Significant advances in artificial intelligence are increasingly driving predictions, decision making and recommendations across many organisations. As digital services become more interconnected, cyber attacks and other outages continue to have the potential to cause widespread disruption and damage.

We will:

- hold ASX to account on the safe and efficient implementation of the CHESS replacement program, ensuring all regulatory requirements continue to be met. We will also oversee planned refreshes of the ASX Trade and ASX 24 trading systems, and upgrades to ASX’s derivatives clearing platforms (the Clearstar program)

- monitor how market intermediaries use AI and assess relevant risk management and governance arrangements

- consult on proposals to modernise and harmonise market integrity rules relating to trading infrastructure, automated order processing and manipulative trading, and to address emerging risks associated with AI and algorithmic trading

- encourage market intermediaries to participate in a self-deployed cyber resilience exercise. We will share learnings to improve cyber resilience capabilities, and

- coordinate ASIC’s work to monitor and engage with market intermediaries on digital assets, tokenisation and decentralised finance. We will update guidance on the regulatory perimeter and encourage preparation for the proposed regulation of digital asset platforms.

Core regulatory activities

In addition to these projects aligned to our strategic priorities, ASIC will continue a wide range of core regulatory activities to monitor and promote market integrity and consumer protection.

ASIC is one of Australia’s most active law enforcement agencies. We will continue to deploy our significant expertise and resources to detect, disrupt, investigate and respond to unlawful conduct in Australian markets.

Conclusion

ASIC remains committed to the promotion of market cleanliness, market integrity and the protection of consumers and investors—irrespective of the changing shape of markets. These objectives are fundamental to maintaining trust in Australia’s financial system.

We encourage you to use these strategic priorities, projects and regulatory activities as a reference for your compliance, supervisory and risk management programs that support your business activities, and to prepare for your interactions with ASIC.

Priorities for 2023-24

ASIC’s continuing strategic priorities, announced last year and detailed in ASIC’s Corporate Plan 2023–27, target the most significant threats and harms in our regulatory environment: product design and distribution, sustainable finance, retirement outcomes and technology risks.

To deliver on these priorities, ASIC will focus on six core strategic projects.

Supporting ASIC’s priorities and core strategic projects, our key areas of regulatory focus for market intermediaries in 2023–24 are:

- Fair and orderly markets

- Cyber, technology and operational resilience

- Product design and distribution

- Governance, accountability, sustainability and risk management

- Implementation of law reform.

Fair and orderly financial markets are essential to ongoing trust, confidence and participation in our financial system. Our supervisory work and enduring enforcement priorities include actions to address misconduct that harms market integrity.

- We continue real-time and post-trade surveillance of trading on Australia’s domestic licensed markets to identify insider trading, market manipulation, disorderly trading and misinformed markets. New tools are being developed and used to increase our detection of complex and novel market abuse matters, market microstructure manipulation and breaches of the market integrity rules. We continue to focus on short sale reporting and regulatory data compliance.

- As gatekeepers, market participants play an important role to lead standards of conduct. We are reviewing participants’ arrangements to prevent and detect misconduct. This includes the adequacy of order filters and controls, governance arrangements including order and trade surveillance alerts, assessment and escalation arrangements and compliance with pre-trade transparency and suspicious activity reporting obligations.

- We continue to review the trade surveillance systems used by market participants in the fixed income, currency and commodity (FICC) markets. We will focus on surveillance alerts for identifying key conduct risks, their assessment and escalation, arrangements for monitoring business communications and deterring misuse of unauthorised devices and apps, and identification of trade surveillance outages and reporting errors.

- We are leveraging our FICC market surveillance system and data analytics to identify market manipulation and other forms of misconduct in FICC markets. We are monitoring commodity derivatives markets with a focus on potential misconduct in gas and electricity markets.

- Use of our new bond surveillance capabilities will inform our surveillance of sustainable finance-related bond issuance, syndicated issues and trading in government, semi-government and corporate bonds.

- We continue to build our oversight of bond markets and consider whether public post-trade transparency would improve liquidity, market efficiency and resilience.

- We monitor the overall health of our financial markets through macro-level market quality measures such as market cleanliness, market liquidity and efficiency statistics.

- We are working to identify and take down investment scams and phishing websites. We are also working with other agencies to coordinate disruption strategies, including our joint leadership of the National Anti-Scam Centre (NASC) investment scam fusion cell with the Australian Competition and Consumer Commission. We continue to expand our communications, including through social media, to help consumers detect and avoid investment scams.

Cyber, technology and operational resilience

We will continue to supervise and engage with market intermediaries to encourage ongoing and timely management of operational risks, and continuous improvement of cyber and operational resilience practices.

- We will be reporting on our cross-industry cyber pulse survey to benchmark market intermediaries’ cyber resilience and develop sectoral insights.

- We are engaging with market intermediaries to promote good practices and support initiatives that enhance cyber resilience, including by leveraging insights from the cyber pulse survey results and heeding international warnings about account intrusions. We will take enforcement action where there are serious failures to mitigate the risks of cyber-attacks and governance failures relating to cyber resilience.

- We are partnering with other financial regulators to support whole-of-government cyber-resilience initiatives and incident responses, where appropriate.

- We are testing compliance with ASIC market integrity rules on technological and operational resilience and will continue to monitor the final steps in market participants’ and market operators’ implementation of the recommendations in Report 708 ASIC’s expectations for industry in responding to a market outage.

Product design and distribution

We will continue to pursue targeted, risk-based surveillance and take action to address poor design and distribution of retail financial products. The design and distribution obligations are intended to help consumers obtain appropriate financial products by requiring issuers and distributors to have a consumer-centric approach to designing and distributing products.

- In September 2023, we reported on our review of how retail OTC derivative issuers are meeting the design and distribution obligations to provide product issuers and distributors with practical observations about making a target market determination and meeting the reasonable steps and review obligations: see Report770 Design and distribution obligations: Retail OTC derivatives.

- We are conducting further targeted surveillance of market intermediaries’ financial product design and distribution practices, increasing our surveillance focus on compliance with the ‘reasonable steps’ obligations.

- We are continuing to examine market intermediaries’ use of digital engagement practices (DEPs) in the marketing and distribution of financial products to identify and address poor industry practice and harmful influences on consumer behaviour and outcomes. Focus areas include gamification, notifications in trading apps, advertising and inducements (including social media), algorithmic trading and social trading features such as copy trading and leader boards.

- We are supporting the development of an effective regulatory framework for crypto-assets focused on consumer protection and market integrity, following the consultation by Treasury.

- We will take action to protect consumers from misconduct associated with crypto-assets within our remit, including those that mimic traditional products but seek to circumvent regulation. We will continue to raise public awareness of the risks of crypto-assets and decentralised finance (DeFi).

- We will take action against market intermediaries who promote and supply unsuitable structured or high-risk products to small businesses.

Governance, accountability, sustainability and risk management

We support market integrity through proactive supervision and enforcement of governance, transparency and disclosure standards. We will also continue to support effective climate and sustainability governance and disclosure.

- Together with the Reserve Bank of Australia, we are closely supervising ASX’s CHESS replacement We are seeking assurances that any gaps or deficiencies are addressed, and stakeholder concerns considered, before ASX pushes forward on its new solution and any other future programs. We will use all currently available measures to ensure that ASX meets regulatory expectations and complies with its obligations under the Corporations Act.

- We will continue to undertake frontline supervision and proactive engagement with market participants, investment banks, securities dealers and issuers of complex products to drive better practices and identify issues early. We conduct risk-based, proactive and reactive surveillance of market intermediaries’ conduct and compliance with financial services laws.

- We will continue to monitor the practices, business structures and product offerings of new and growing online trading providers. We will continue to take action where our expectations have not been met, including in relation to the supervision of authorised representatives, high-risk offers, the use of misleading and deceptive statements and client money handling practices.

- We will continue to monitor the development of artificial intelligence, data analytics and machine learning to understand the threats and opportunities for regulated entities and markets.

- We will continue to actively monitor the progress and effective completion of market intermediaries’ remediation plans and independent expert reviews (e.g. court enforceable undertakings, licence conditions and court orders).

- We continually monitor the financial strength of market intermediaries, including through testing compliance with capital and financial resource requirements using enhanced risk indicators and risk-based surveillance. We will also conduct targeted surveillance of arrangements for handling client money and safeguarding client assets.

- We will monitor sustainability-related disclosure and governance practices of our regulated populations, including listed companies, managed funds, service providers and sustainable finance bonds. We will take action against serious misconduct, including greenwashing and other false or misleading statements.

- We will continue our frontline supervision of market operators, including new product offerings (e.g. proposed equity listings on Cboe Australia). We will ensure that market operators meet regulatory expectations by promoting competition and fair, orderly and transparent markets.

Implementation of law reform

We will support market intermediaries’ implementation of law reform. We will continue to provide guidance to industry about how we plan to administer and enforce the law – especially for new obligations.

- We will continue to work with market intermediaries to ensure the objectives of the reportable situations regime are met, including by implementing solutions that will improve the consistency and quality of reporting practices and conducting targeted surveillance of entities with relatively low numbers of reportable situations. We will develop and implement a framework for ongoing publication of information about the reports received.

- We will continue to work with APRA to implement the Financial Accountability Regime by providing guidance, engaging with industry and developing effective registration and other processes.

- We have extended until 31 March 2025 transitional relief for foreign financial service providers (FFSPs) from the requirement to hold an Australian financial services (AFS) licence when providing financial services to Australian wholesale clients. We will support Treasury as it settles its policy following consultation on exposure draft legislation to provide AFS licensing exemptions for certain FFSPs.

- We will consult on automated order processing rules for futures market participants and on minor amendments to false or misleading appearance rules for securities and futures market participants.

- We are aligning the over-the-counter (OTC) derivatives trade reporting requirements in Australia with international requirements, including the unique transaction identifier, the unique product identifier and critical data elements, in preparation for the new requirements due to commence on 21 October 2024.

- We will continue to promote the development of international standards and better practices through our participation in IOSCO working groups and liaison with other local and international regulatory agencies. Areas of focus include sustainability-related financial disclosure standards, carbon markets, pre-hedging practices, retail market conduct, DEPs, crypto assets and DeFi, vulnerabilities in markets for leveraged loans and collateralised debt obligations and emerging retail market conduct issues.

- We will continue to publish a six-monthly regulatory developments timetable with expected timeframes for ASIC’s regulatory work. To stay informed about regulatory developments and issues affecting market intermediaries, we also recommend subscribing to our monthly newsletter and participating in our quarterly Market Liaison Meetings.

Conclusion

We encourage you to use these priorities as a reference tool for your compliance, supervisory and risk management programs, and to prepare for your interactions with ASIC.

We remain committed to using the full range of ASIC’s powers, including enforcement action, to preserve the integrity of the Australian financial markets. Our updated enforcement priorities for 2024 will be published later in the year to align with the changing economic conditions and emerging trends and risks outlined in ASIC’s corporate plan.

Priorities for 2022-23

ASIC’s strategic priorities are detailed in ASIC’s Corporate Plan 2022–26.

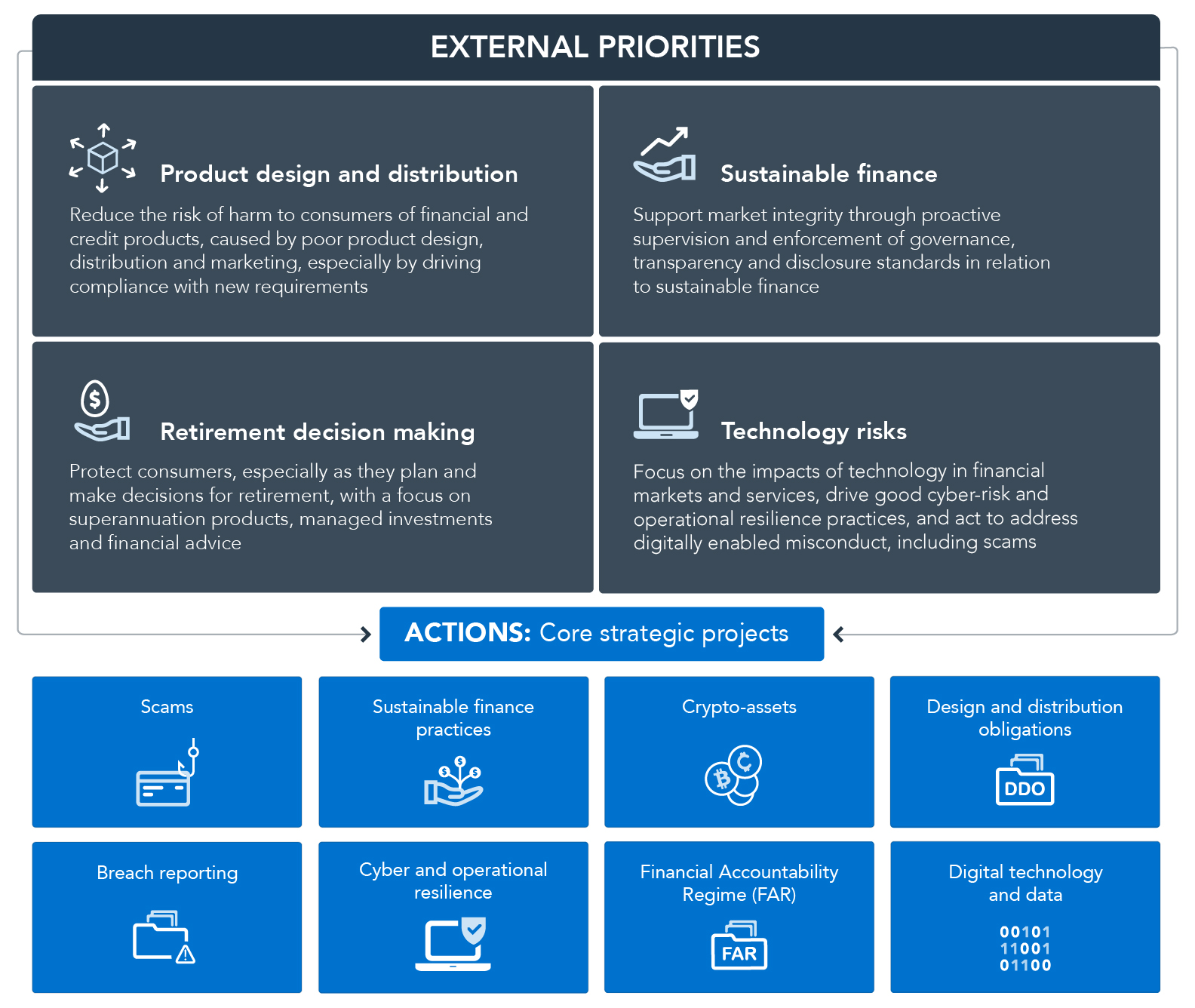

Our external priorities target the most significant threats and harms in our regulatory environment. To deliver on these external strategic priorities, ASIC will focus on eight core strategic projects. (Click image to enlarge)

ASIC's external strategic priorities - text version

External priorities

- Product design and distribution: Reduce the risk of harm to consumers of financial and credit products, caused by poor product design, distribution and marketing, especially by driving compliance with new requirements.

- Sustainable finance: Support market integrity through proactive supervision and enforcement of governance, transparency and disclosure standards in relation to sustainable finance.

- Retirement decision making: Protect consumers, especially as they plan and make decisions for retirement, with a focus on superannuation products, managed investments and financial advice.

- Technology risks: Focus on the impacts of technology in financial markets and services, drive good cyber-risk and operational resilience practices, and act to address digitally enabled misconduct, including scams.

Core strategic projects

- Scams

- Sustainable finance practices

- Crypto-assets

- Design and distribution obligations

- Breach reporting

- Cyber and operational resilience

- Financial Accountability Regime (FAR)

- Digital technology and data

Supporting ASIC’s priorities and core strategic projects, our most significant planned activities for supervision of market intermediaries in 2022–23 is focused on:

- Cyber, technology and operational resilience

- Fair and orderly markets

- Product design and governance

- Governance, accountability, sustainability and risk management

- Implementation of law reform

Cyber and operational resilience among market intermediaries minimises the risk of disruption from cyber attacks and operational failures and promotes confidence in markets.

- We are implementing a cross-industry self-assessment to benchmark market intermediaries’ cyber resilience and develop sectoral insights.

- We will conduct risk-based reviews of cyber and operational resilience among market intermediaries, including reviews of supervisory controls for remote working arrangements, and compliance with new market integrity rules on technological and operational resilience that apply from March 2023.

- We will monitor market participants’ and market operators’ implementation of the recommendations set out in Report 708 ASIC’s expectations for industry in responding to a market outage.

- We will engage with market intermediaries on their preparedness for and implementation of exchange trading platform upgrades.

- We are closely supervising ASX’s Clearing House Electronic Subregister System (CHESS) replacement project so that it will continue to provide reliable clearing and settlement services for the Australian cash equity market. For market intermediaries, we will oversee their preparation for the new CHESS system, focusing on testing arrangements to limit downstream issues and any implications for clients.

The efficient operation of fair and orderly financial markets is the cornerstone of our economy – and is essential to ongoing trust and confidence in our financial system.

- We are undertaking real-time and post-trade surveillance of trading on Australia’s domestic licensed markets to identify insider trading, market manipulation, disorderly trading, and misinformed markets. We are applying new tools to increase our detection of complex and novel market abuse matters.

- We are reviewing market participants’ arrangements to prevent and detect misconduct as part of their important role as gatekeepers. This includes consideration of the adequacy of order filters and controls, related governance around order and trade surveillance alerts (including their assessment and escalation) and compliance with suspicious activity reporting obligations.

- We will review market intermediaries’ trade surveillance systems with a view to releasing guidance on better practices.

- We are conducting surveillance of carbon and energy derivative markets and are implementing a new memorandum of understanding with the Australian Energy Regulator to address concerns about misconduct in gas and electricity markets.

- We are further enhancing our fixed income, currency and commodity (FICC) market surveillance system and data analytics. We are using our new bond surveillance capabilities, with a focus on green bonds, syndicated issues and secondary trading in government, semi-government and corporate bonds.

- We are undertaking a thematic review of artificial intelligence/machine learning (AI/ML) practices and associated risks and controls among market intermediaries and buy-side firms, including the implementation of AI/ML guidance issued by the International Organization of Securities Commissions (IOSCO).

- We will consider whether the automated order processing market integrity rules should be extended to futures market participants, and whether the rules should be updated to reflect developments since they were made.

- We are conducting proactive surveillance of debt capital markets issuance to test against our expectations for conduct and controls in Report 668 Allocations in debt capital market transactions.We continue to monitor and test allocation practices for selected equity raising transactions.

- We will align the over-the-counter (OTC) derivatives trade reporting requirements in Australia with international requirements, including the Unique Transaction Identifier, the Unique Product Identifier and Critical Data Elements.

- We are enhancing how we identify, quantify and disrupt scams through a data-informed approach. We are working with other regulators and law enforcement agencies, both domestic and overseas, to disrupt scams and coordinate enforcement strategies. We are improving our communications and consumer education, including through social media, to help consumers be more aware of scams and how to identify them.

The design and distribution obligations came into effect on 5 October 2021. These obligations require financial product issuers to design products that meet the needs of consumers and are targeted to the right consumers.

- We are conducting risk-based surveillance of market intermediaries’ financial product design and distribution practices, including:

- design and approval of new products

- issuers’ reviews of target market determinations (TMD) and distribution arrangements

- notifications of significant dealings inconsistent with TMDs

- supervision of authorised representatives

- marketing governance (including social media)

- assessment of client outcomes by distribution channels.

- We are reviewing market intermediaries’ use of digital engagement practices in trading apps and their potential influence on consumer behaviour and outcomes, including algorithmic and copy trading, leader boards, gamification, inducements and other behavioural levers.

- We are undertaking surveillance of crypto-asset offerings by market intermediaries that fall in our remit (e.g. derivatives, managed funds and debentures) for potential misleading or deceptive conduct that may result in consumer harm. We will also raise public awareness of the risks of crypto-assets and decentralised finance (DeFi).

- We are implementing and monitoring the regulatory model for exchange traded products with underlying crypto-asset exposures.

- We will take enforcement action to address poor product design and distribution practices that result in consumer harm, including misleading, predatory or hawking tactics.

We support market integrity through proactive supervision and enforcement of governance, transparency and disclosure standards.

- We will continue to undertake frontline supervision and proactive engagement with market participants, investment banks and securities dealers to drive better practices and early identification of issues. We conduct proactive and reactive surveillance of market intermediaries, securities dealers and corporate authorised representatives.

- We will increase our engagement with new and growing market intermediaries and undertake thematic reviews of identified risks (e.g. client money handling, new product approval processes and marketing governance).

- We are actively monitoring the progress and effective completion of market intermediaries’ remediation plans and independent expert reviews (e.g. court enforceable undertakings, licence conditions and court orders).

- We are monitoring the financial strength of market intermediaries, including through testing compliance with capital requirements using enhanced risk indicators and risk-based surveillance. We are also reviewing arrangements for handling client money and safeguarding client assets.

- We will monitor sustainability-related disclosure and governance practices of listed companies, managed funds and green bonds and take enforcement action against misconduct, including misleading marketing and greenwashing.

- We willpublishreports on better and poorer practicesobserved in ourreviews of wholesale market intermediaries’ management of conflicts of interest and fixed income market practices. We will continue toengage with industry bodiesto promote development of good industry standards.

- We will contribute to IOSCO’s work on sustainable finance, hidden leverage, collateralised loan obligations and leveraged loans, OTC trade reporting, operational resilience and retail market conduct.

- We will continue our reviews of whistleblower programs, corporate finance transactions and the LIBOR transition.

We will support market intermediaries’ implementation of recent and upcoming law reform. We will continue to provide guidance to industry about how we plan to administer and enforce the law – especially for new obligations.

- We are aware the new reportable situations regime has been challenging to implement. We continue to closely monitor the operation of the new regime to support industry with the practical implementation of the new obligations. We will work with AFS licensees to implement solutions to improve the consistency and quality of reporting practices.

- We have updated our market integrity rule guidance following recent rule amendments, including to the technological and operational resilience rules and capital rules.

- Subject to the passage of legislation, we will work with APRA to facilitate a smooth implementation of the Financial Accountability Regime, including implementing a coordinated, risk-based approach to registration activities under the regime.

- We are supporting the Government’s development of Foreign Financial Service Provider regulation and transitional arrangements.

- We will support the development of a regulatory framework for crypto-assets and work with domestic and international peers to monitor risks, develop coordinated responses to issues and develop international policy regarding crypto-assets and DeFi.

- We will promote the development of international standards and better practices through our participation in IOSCO working groups and liaison with other local and international regulatory agencies.

- We will seek your feedback on ways we can improve regulatory efficiency and reduce red tape. We will continue to provide relief, where appropriate, to participants in capital markets and the financial services industry to facilitate business, promote innovation and support the Australian economy.

Conclusion

We encourage you to use this letter as a reference tool for your compliance, supervisory and risk management programs, and to prepare for your interactions with ASIC. To stay informed of regulatory developments and issues affecting market intermediaries, we recommend subscribing to our monthly newsletter and participating in our quarterly Market Liaison Meetings.

Priorities for 2021-22

ASIC’s strategic priorities are detailed in ASIC’s Corporate Plan 2021–22.

Our four external priorities target the most significant threats and harms in our regulatory environment:

- Promoting economic recovery

- Reducing risk of harm to consumers

- Supporting enhanced cyber resilience and cyber security among ASIC’s regulated population

- Driving industry readiness and compliance with standards set by law reform initiatives.

We recognise that market intermediaries are currently facing many challenges, including from the impacts of the COVID-19 pandemic and several important legislative reforms taking effect this financial year. We are adapting our work program to reduce the number of reviews of market intermediaries and providing regulatory relief where appropriate. While we are focused on supporting business and the economic recovery, we will take enforcement action where there is evidence of misconduct and it is in the public interest to do so.

The projects outlined below represent the most significant pieces of work relating to ASIC’s supervision of market intermediaries and is not an exhaustive list.

Our work in 2021-22 is focussed on four main areas:

- Reducing risk of harm to consumers

- Supporting enhanced cyber and operational resilience

- Maintaining high industry standards

- Enhancing our market surveillance and data analytics

Reducing the risk of harm to consumers

Historically low interest rates and the ongoing search for yield have inflated retail investor risk appetite and stimulated scam activity. While we seek to quickly identifying and shut down scams, we encourage market intermediaries to raise awareness among their clients of the heightened risk environment.

Assessing the evolution of retail products and distribution strategies

- We are working to better understand the extent to which trading apps are gamifying trading or encouraging excessive trading by retail investors.

- We are consulting on proposals to enhance the application of market integrity rules for payment for order flow practices through CP 347.

- We are reviewing market practices in relation to copy trading, including its outcomes for investors and the application of financial services laws.

- We are reviewing the adequacy of monitoring and supervision arrangements licensees have for their corporate authorised representatives.

- We will seek to improve disclosure about the risk of pooling of client cash and security holdings using omnibus Holder Identification Numbers, and the structure and risks associated with fractional share offerings.

Embedding strategies to monitor social media advice and influence on retail investment decisions

- We are engaging with social media platforms, forum moderators and financial influencers or ‘finfluencers’ to consider market practices, the application of financial services laws and drive behavioural change.

- We are embedding tools and undertaking reviews of social media to detect unlicensed advice to retail investors.

- We are developing educational content for retail investors, including through social media to connect with investors and disseminate real-time warnings.

- We are enhancing our social media monitoring and network analytics capability to identify more connections, as well as coordinated activity that may harm market integrity or contribute to market manipulation.

Product Intervention Orders

- In 2021, Product Intervention Orders came into effect for Contracts for difference (CFDs) and binary options.

- From 29 March 2021, ASIC’s product intervention order relating to CFDs (CFD PIO) strengthened protections for retail clients by restricting CFD leverage to reduce the size and speed of losses, standardising margin close-out arrangements, protecting against negative account balances and prohibiting the offer of certain inducements to retail clients.

- ASIC made a product intervention order banning the issue and distribution of binary options to retail clients, with effect from 3 May 2021.

- We are closely monitoring these markets to ensure compliance with these orders and collecting data to consider whether these product intervention orders should be extended or made permanent.

Supporting enhanced cyber and operational resilience

Cyber resilience

- We are supporting enhanced cyber resilience and cyber security among ASIC’s regulated population, in line with the whole-of-government commitment to mitigating cyber security risks, including to raise awareness of cyber issues.

- We are probing and assessing the cyber resilience of our regulated population. We take a risk-based approach to target entities for assessment utilising our cyber risk rating framework.

Operational resilience

- We are assessing and monitoring the operational resilience of market intermediaries, with a focus on:

- the changing operating environment through the COVID-19 pandemic and increase in remote and hybrid working

- preparedness to respond to any future market infrastructure outages or incidents

- industry’s readiness for LIBOR transition and CHESS replacement

- ongoing monitoring of the technology and operational risk governance practices of market intermediaries and undertaking on-site reviews as appropriate.

- We are also looking to finalise and implement new market integrity rules for market participants and operators focussed on systems and controls.

Maintaining high industry standards

Industry readiness and compliance with standards set by law reform taking effect in October 2021

- We are engaging with market intermediaries on their preparedness and implementation of reforms taking effect in October 2021. The reforms include:

- design and distribution obligations

- breach reporting to ASIC

- restrictions on the unsolicited selling of financial products (hawking)

- how disputes are managed internally in firms

- reference checking and information sharing requirements for financial advisers and brokers.

- ASIC will take a reasonable approach in the early stages of these reforms provided industry participants are using their best efforts to comply (see 21-213MR).

- We will undertake risk-based reviews of compliance with the new obligations around the second half of the financial year, including to test whether Target Market Determinations and frameworks for review of product design and distribution are satisfactory.

Setting and testing standards in other areas

- We are preparing for the implementation of the Financial Accountability Regime in 2022.

- We are monitoring the financial strength of market intermediaries, including through safeguarding retail client monies and implementation of new capital adequacy requirements.

- We will continue to review the appropriateness of advice and control frameworks for the provision of advice by market intermediaries and may provide guidance to raise standards.

- We are seeking to improve and align Australia’s reporting of OTC derivative transactions with international standards by consulting on harmonised trade reporting rules.

- We are also undertaking supervisory activities that address key themes such as technology and systems, operational resilience and internal audit, including use of targeted onsite reviews when appropriate.

Equity and Debt Capital Market raisings

- We are continuing to test the management of conflicts of interest by market intermediaries providing research and corporate work, as well as any potential conflicts in making allocations in equity and debt raisings. We do this through ongoing monitoring of transaction activity, media commentary and complaints relating to capital raising transactions.

Enhancing our market surveillance and data analytics

Fixed Interest, Currency and Commodity (FICC) market surveillance and data analytics

- We are enhancing our FICC market surveillance capability, by ingesting and interrogating a broader range of data, to keep abreast of changing market dynamics and indicators of poor conduct.

- We have a focus on emerging harms from the search for yield in the low yield environment, as well as insider trading and possible manipulation of lower/sub investment grade bonds.

- We are also seeking to identify poor behaviour in short term money markets, domestic/cross currency swap and futures markets.

Securities market: real-time and post-trade surveillance

- ASIC undertakes real-time surveillance of trading on Australia's domestic licensed markets. This includes identifying and taking action against insider trading, market manipulation, disorderly trading and misinformed securities markets. This financial year, we are focussed on:

- strategies that artificially move prices and induce other investors to trade at artificial levels. This includes momentum ignition, ramping and pump and dump. We are especially focused on the role of social media influence

- activist short selling and short squeezes, with a key focus on maintaining market integrity, an informed market and addressing information asymmetry

- cross-market and product manipulation and insider trading (e.g. trading across shares, CFDs and swaps)

- suspicious activity reporting and improving the number and quality of these important sources of intelligence.

Conclusion

We encourage you to use this letter as a reference tool for your compliance, supervisory and risk management programs, and to prepare for your interactions with us. We also recommend you subscribe to our free monthly Market Integrity Update, to stay informed of regulatory developments and issues affecting market intermediaries.

Priorities for 2019-20

- To realise ASIC’s vision for a fair, strong and efficient financial system for all Australians, seven principal strategic priorities were developed by ASIC for the year 2019–20.

- This letter outlines how we are implementing these strategic priorities in our supervision of market intermediaries.

- Plan for the year ahead by assessing your governance framework against these priorities.

In our supervision of market intermediaries, we have focussed on three of these strategic priorities:

- High-deterrence enforcement action

- Improving governance and accountability

- Protecting vulnerable consumers.

While the projects outlined below are not an exhaustive list of what we plan to do, they represent the most significant pieces of work that we will undertake in supervising market intermediaries to achieve our strategic priorities.

1. Fixed income, currencies and commodities (FICC) markets – managing threats to the real economy

Summary

- Discrepancies exist in the practices of FICC market participants and market operators across supervision and surveillance, risk controls, governance, conflict management and culture.

- Our FICC strategy addresses threats to these markets, which may cause harms to the real economy and consumers.

- We’re expanding our oversight of these markets through proactive surveillance, enhancing standards and driving behavioural change.

Background

Fixed income, commodities and currency (FICC) markets are global, directly link to the real economy, and are considerably larger than exchange traded markets. These are wholesale markets, but many of the transactions are to fund or manage risk for businesses and superannuation funds.

Fixed income markets generally have lower transparency than their equity equivalents. Low visibility of the pricing and dealing mechanisms used by market professionals means that investors can’t proactively validate the effectiveness of the organisation’s controls, which are used by firms to maximise opportunities for their clients.

Activities

- Targeted transaction reviews – We’re continuing our program of targeted reviews of large transactions to assess if the intermediaries are complying with the law, are fit for purpose, and are delivered fairly and honestly.

- Enhanced oversight of bank bill markets – Following the implementation of the new regulatory framework for benchmarks, we’re increasing our focus on the bank bill market and the formation of the Bank Bill Swap Rate (BBSW).

- Continue expanding our program of onsite reviews – We’ll continue to undertake onsite reviews of a selection of intermediaries’ fixed income businesses, and also undertake reviews of intermediaries’ conflicts of interest arrangements. We’ll use these to assess non-compliance with the law and improve behaviours in the market.

- Foreign Exchange (FX) and BBSW Court Enforceable Undertakings – We’ll continue to monitor compliance with FX and BBSW court enforceable undertakings and court orders.

- Review allocation practices for debt capital markets (DCM) transactions - Building on our findings in REP 605 Allocations in equity raising transactions, we’re undertaking a review of market practice for allocations in DCM transactions and co-leading work with international peers through the International Organization of Securities Commissions (IOSCO).

- Monitor impact of global LIBOR transition – We’re undertaking work to understand and monitor intermediaries’ management of contracts that currently reference LIBOR and need amending to a new reference rate.

- OTC trade reporting – We’re continuing work to improve existing data quality and address non-compliance by reporting entities.

2. Enhanced supervision for market intermediaries

Summary

- We’re continuing to embed and expand our enhanced supervision model for the most high-risk and complex entities.

- We’re also tailoring our proactive and reactive supervision approach for intermediaries assessed as medium and low risk.

- We expect all firms to have a professional and robust approach to conduct – to operate with integrity and to act in the best interest of their clients.

Background

We’ll continue to implement our enhanced supervision model for market intermediaries. Firms that have the most significant market presence, or pose the greatest risk to our priorities, should expect a more intensive level of supervision across all areas of their business. We’ll test that market intermediaries meet their regulatory requirements and require remediation of non-compliance.

We’ll continue to undertake thematic and sector reviews to inform future surveillance work and the establishment of regulatory expectations. We also expect firms to have a professional and robust approach to conduct, including:

- proactively identifying conduct risks

- encouraging accountability for conduct across all areas of the firm

- supporting staff to improve conduct

- board and executive oversight of conduct, and a focus on the conduct implications of the decisions that they make.

We’ll periodically test these themes and we expect firms to demonstrate how they have addressed them.

Activities

Culture and conduct – We’ll assess the strategy, culture and behavioural drivers of conduct of market intermediaries, including through our conduct review themes.

Breach reporting – We’ll test compliance with breach reporting obligations.

Technology and operational risk management – We’ll undertake reviews to check that risk management is embedded in planning, project management and performance management in technology, and other operational risk areas.

Coordination with global regulatory authorities – We work closely with our regulatory colleges around the world to achieve consistent regulatory outcomes and to identify emerging regulatory concerns. We also participate in international and domestic supervisory colleges to inform our supervisory approaches for major banking and financial groups.

3. Risky OTC derivatives – protecting vulnerable retail consumers and raising standards

Summary

- Certain OTC derivatives products are aggressively marketed to retail investors, resulting in significant investor losses.

- We’ll test that providers of retail OTC derivatives products comply with their regulatory requirements, including when providing services outside Australia.

- We’ll also consider using the range of our regulatory and enforcement powers where there are retail OTC derivatives products, issuers or marketing that is causing consumer harm.

Background

OTC derivatives are highly risky for most retail investors, often resulting in significant investor losses. There have also been several recent instances of retail OTC derivatives providers not complying with their regulatory requirements.

We’re seeking to protect retail investors by educating them about the risks of trading these products, holding individuals and licensees to account for poor conduct, and raising industry standards.

Activities

- Industry benchmarking – We will examine and benchmark the size and nature of the Australian market, and the extent of investor losses and other harms.

- Onsite surveillance – We’ll undertake onsite surveillances of product issuers, with a focus on cold calling and pressure selling tactics, licensees acting outside the scope of their license, and misleading and deceptive conduct.

- Improve industry standards – We’ll seek to raise standards in the retail OTC derivatives industry, including by consulting on implementing the IOSCO Regulatory toolkit to enhance conduct standards.

- Consider use of a range of our regulatory and enforcement powers – Where we see that products or practices in this sector have resulted in, or are likely to result in, significant consumer harm then we will consider which of the range of powers available to us should be used to address this harm and we will also address past misconduct.

- Remind retail OTC derivatives providers to comply with foreign law – Following the April publication of ASIC 19-088MR Some AFS licensees may be breaking overseas laws, we’ll continue to test with firms that they comply with foreign regulatory requirements, and we may act against firms that do not.

4. Other priority projects

- Safeguarding retail client money – We’ll test market intermediaries’ compliance with client money requirements, including as part of our enhanced supervision under item 2. We’ll undertake a review of practices and provide practical guidance where needed.

- Suspicious activity reporting – We want to improve the quality and quantity of suspicious activity reports to ASIC, particularly in wholesale FICC markets. These reports are a valuable source of information, and their improved use will strongly contribute to our ability to identify and action market misconduct.

- Checking intermediaries are prepared for ASX CHESS replacement - ASX is replacing the CHESS cash equities clearing and settlement system with a platform based on a private permissioned distributed ledger. Market intermediaries should be planning now and making the necessary arrangements for the implementation of the replacement system to facilitate a smooth industry transition. We’ll be monitoring this process. We will also be supervising ASX’s implementation of the system against its clearing and settlement facility licence obligations.

- Intermediary resilience and capital adequacy – We’ll consider whether any changes are needed to our approach for early detection of the potential failure of market intermediaries and the steps we and they take to mitigate client losses. The protection of client assets is our priority, in addition to the potential impact of failures on market integrity.

- Financial advice by stockbrokers – We’ll continue to consider the application of financial advice laws to stockbrokers and review the appropriateness of advice and control frameworks for the provision of advice by market intermediaries.

- Improving governance, accountability and compliance – We’ll assess the compliance and broader non-financial risk management models across a sample of intermediaries (including those subject to enhanced supervision – item 2) and market operators and determine if changes are needed to industry standards or our supervisory approach.

- Equity capital raising allocations and sell-side research – We’ll test market intermediaries’ implementation of Regulatory Guide 264 Sell-side research, to check compliance and to better understand how the arrangements are applied in practice.

- Trade surveillance – We’ll continue to rigorously pursue market misconduct, including market manipulation and insider trading.